States take BEAD applications while Washington mulls program changes

Washington, DC (February 24, 2025) - While the Broadband Equity, Access, and Development (BEAD) program has faced some headwinds lately in Washington, the states remain as active than ever. Thirty states are taking project applications now, or have completed at least one round of project applications, including the three — Louisiana, Delaware, and Nevada — which have completed their subgrantee selection and have gotten their Final Proposals approved.

Many other states are taking “prequalification” (variously called “qualification,” “pre-application,” etc.) submissions — the means by which internet service providers (ISPs) are vetted as organizations before specific projects get submitted and evaluated. While a few states are still focused on completing their BEAD challenge processes, the vast majority are well into subgrantee selection.

This rapid progress in the states — as welcome as it is after three years in which the BEAD program worked through a series of planning stages — creates a challenge for the BEAD program’s new leadership in Washington, D.C. Recent public statements by newly confirmed Secretary of Commerce Howard Lutnick and National Telecommunications and Information Administration (NTIA) Administrator nominee Arielle Roth indicate that they have some ideas about how BEAD should change. But it’s tricky to modify the BEAD program while it’s in flight.

The next few weeks will reveal whether the new leadership manages to correct course to align BEAD with their vision without disrupting its recent rapid progress.

BEAD vs. the funding freeze?

On January 27, 2025, Matt Vaeth, the General Counsel and, at the time Acting Director, of the U.S. Office of Management and Budget (OMB), issued memo M-25-13 (link downloads a PDF), which required the review of all federal funding to purge support for, “Marxist equity, transgenderism, and green new deal social engineering,” and included the statement that “to the extent permissible under applicable law, Federal agencies must temporarily pause [emphasis in original] all activities related to obligation or disbursement of all Federal financial assistance,” starting January 28, 2025, at 5 p.m. Broadband industry stakeholders immediately began worrying that the language would appear to apply to the BEAD program.

On January 28, just before the deadline, U.S. District Judge Loren L. AliKhan temporarily blocked the funding freeze until February 3. OMB rescinded the memo on the following day. Soon after, however, the White House said the funding freeze was still in force.

On February 3, the judge extended the restraining order on the funding freeze. On February 10, U.S. District Judge John J. McConnell found that the executive branch was failing to comply with an earlier ruling against the funding freeze. Litigation remains ongoing.

States may be safe, since most of them requested 100% of their BEAD funds in their approved Initial Proposals. They don’t have a right to spend the majority of these funds, however, until their Final Proposals are also approved. Final Proposal submission is the next major touchpoint with the NTIA for most states, with the nearest deadlines in April, as shown below:

Figure 1: Next 10 states with Final Proposals due

Hopefully, by the time these deadlines are reached, the legal status of the funding freeze will be clearer. As Connect Humanity recently observed, “To expand broadband, rural communities need clarity on government funding.”

Should BEAD support ‘broadband infrastructure’ only?

An important exchange with Senate Majority Leader John Thune (R-S.D.), which took place during Howard Lutnick’s Senate confirmation hearing, may indicate another impending change to the BEAD program.

“And,” said Sen. Thune, “will you also work to ensure that this funding is only used for actual broadband infrastructure builds?”

“Absolutely,” Lutnick emphatically answered.

If Lutnick follows through on this promise, that will represent an important and significant BEAD policy change.

Since it was created by Congress, BEAD has been focused on last-mile deployment, starting with unserved and underserved locations, then community anchor institutions. But after universal broadband coverage is on track, leftover funds could be used for a variety of different broadband-adjacent purposes.

The statute itself listed three further purposes: a.) data collection, broadband mapping and planning; b.) installation of broadband or Wi-Fi in apartment buildings, and c.) broadband adoption and device programs.

The statute also allowed BEAD funds to be expended for “any use determined necessary by the Assistant Secretary” — the NTIA — “to facilitate the goals of the Program.” Accordingly, in the BEAD NOFO, the NTIA included a 12-item list of allowable uses for BEAD non-deployment funds, with inclusive language inviting further ideas from states, subject to approval. Some of these allowable uses would qualify as infrastructure, but others don’t.

Of the three states with approved Final Proposals so far, Nevada had no BEAD funds to spare. But Delaware can expect around $70 million, and Louisiana over $500 million. Both states articulated diverse plans for the money, some of which should probably qualify as infrastructure investment, while others clearly don’t.

For example, Louisiana has plans for scaling digital K-12 programming, and for helping small businesses to upskill their workforces. Delaware also has plans for a workforce investment and upskilling program. To judge from their Initial Proposals, many other states are on track to create similar programs with BEAD funds, if, as is likely in many states, they don’t need all their funds for last-mile deployment.

For BEAD to refocus on broadband infrastructure builds would, of course, require more than a verbal statement by Commerce Secretary Lutnick in a committee hearing. The normal process would be for the NTIA to issue explicit guidance. Ideally, states would be given more time to adjust to the new policy, especially since funding infrastructure requires careful planning to ensure that funds are spent wisely.

In the vein of other personnel changes, Arielle Roth is poised to become the next NTIA Administrator. Roth, who has served at both the Federal Communications Commission (FCC) and on the staff of Senate Commerce Committee Chairman Ted Cruz (R-TX), has been a critic of BEAD in the past for its “extra-legal requirements” and “woke social agenda.” Congratulatory statements for her nomination were issued by WIA, Comcast, FCC Chairman Carr, USTelecom, and Charter — among others.

With this expected change in leadership, suggested improvements to the BEAD program have been submitted by Texas Comptroller Hegar to Sen. Ted Cruz, from Gov. Jeff Landry of Louisiana to Commerce Secretary Howard Lutnick, from the Advanced Communications Law and Policy Institute at New York Law School, and from USTelecom to the President, full of suggestions how to streamline the program — with many focused on the removal of the BEAD “low-cost service option” (LCSO).

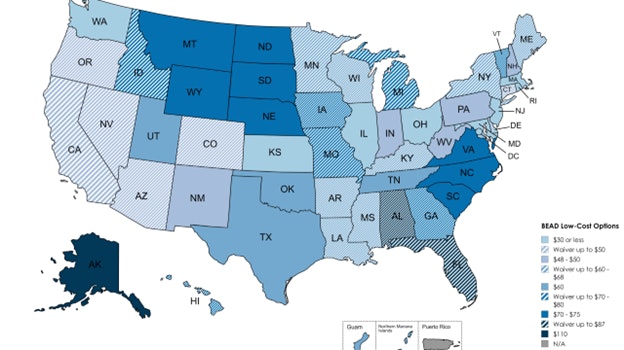

The low-cost service option (LCSO)

As BEAD networks get built, BEAD subgrantees will be required to offer a low-cost service option to means-tested eligible subscribers who reside in the footprint of their BEAD-funded networks. Jake Varn of Pew Charitable Trusts compiled a national map of state BEAD LCSOs:

Figure 2: BEAD low-cost service options by state

The LCSO derives from the Infrastructure Investment and Jobs Act (IIJA) statute itself, which Congress passed in November 2021. It states that BEAD subgrantees “shall offer not less than one low-cost broadband service option for eligible subscribers,” and goes on to describe how states should define a LCSO in consultation with the NTIA.

Expanding on this, the NTIA, in its BEAD NOFO, defines a list of criteria that will make households eligible for the BEAD LCSO, including household income below 200% of the Federal Poverty Line and receipt of a variety of public benefits.

The NOFO also offers a suggested definition of the LCSO, based on a $30/month price. At the time, that price combined with the $30/month subsidy that was available through the Affordable Connectivity Program (ACP) would have implied free internet service for eligible subscribers living in BEAD areas. As indicated by the map above, quite a few states adopted this definition. However, more did not.

One reason for their reluctance was resistance from the broadband industry. While that resistance isn’t surprising — naturally, ISPs don’t want to be required to sell internet service for less than they’d like to charge — it helps to unpack the resistance to better understand the ramifications for the BEAD program. The LCSO affects the basic economics of BEAD in ways that may raise the program’s cost to taxpayers more than it hurts the profits of ISPs that receive BEAD awards.

Figure 2 shows the basic economics of a BEAD grant, and how a one-off grant can, if all goes well, permanently solve an internet access problem.

Figure 3: BEAD grants economics

In Figure 2, the blue bar represents capital expenditure, or “capex” — i.e., what the ISP needs to spend to build a broadband network and make it operational. The green bar represents future customer revenues that the network will earn, translated into current dollars using the finance concept of “present value” (PV). In the example shown, the PV of customer revenue is less than capex, which ensures that the network shown will need subsidies to get built.

Also driving the need for subsidies is the yellow bar, representing the PV of operating and maintenance expenses, or “opex.” The difference between PV of revenue and PV of opex, expressed in the orange bar, determines what a rational private ISP would be willing to invest in the network from its own cash.

The BEAD program is needed because, for millions of locations across America, the orange bar is shorter than the blue bar. Private willingness to invest is less than capex, so the network won’t be built without a subsidy.

The BEAD program can succeed wherever the yellow bar is shorter than the green bar. If PV of revenue exceeds PV of opex, then once the capex hurdle is cleared and the network is built, the ISP can keep operating the network profitably, without ongoing subsidies. If not — if the yellow bar representing PV of opex is longer than the green bar representing PV of customer revenue — then no BEAD subsidy will make the project sustainable.

BEAD only funds capex, so it can only fix broadband coverage problems when they’re caused by a capex hurdle. If the network would require ongoing operational subsidies to cover its costs, then BEAD isn’t built for that.

How are the economics of BEAD grants affected by the LCSO? That is shown by Figure 3, in which the darker-shaded bars represent values where the LCSO is set high (or doesn’t exist), while the lighter-shaded bars represent a lower LCSO scenario:

Figure 4: How the low-cost service option (LCSO) affects BEAD grants economics

With a lower LCSO:

- PV of revenue is reduced. The ISP makes less money because it has to charge less to many customers.

- PV of opex stays the same or rises. Figure 3 shows no change in opex. Alternatively, opex might increase because of a.) higher take rates, and b.) the administrative burden of means testing subscribers for LCSO eligibility.

- Willingness to invest falls. ISPs who foresee that the LCSO will reduce their revenues (and maybe raise their costs, too) will be less willing to invest private matching capital.

- The BEAD grant must get bigger. The more the LCSO reduces future customer revenues, the larger the BEAD grant will need to be to induce participation.

In some cases, a low LCSO might render a project commercially unsustainable altogether. In other cases, it might push the subsidy requirements for fiber too high and cause state broadband offices to opt for projects that use less expensive technologies.

Also, BEAD generally requires a 25% match, so if a low LCSO reduces private willingness to invest below that level, say to 10% of capex, then the project might become non-viable under BEAD rules even if it could be commercially sustainable once built. But private ISPs’ reluctance to put significant skin in the game is a sign that a project is at risk of unsustainability.

Figure 3 shows, incidentally, why a lower LCSO might not reduce the profitability of BEAD projects for subgrantees. If a low LCSO forces BEAD applicants to ask for larger grants up front, less revenue for less matching capital investment might leave ROI the same.

If the new NTIA leadership heeds the advice to eliminate the LCSO, that will help the BEAD grants to achieve more last-mile deployment value per federal investment subsidy dollar, and it will make it easier for states to achieve universal broadband coverage.

On the other hand, the internet service deployed will be less affordable to some people who need it. An alternative would be to adjust the LCSO so that the discount could be on a lower service tier, e.g., for 25 Mbps download/3 Mbps upload instead of 100/20 Mbps speeds. That would encourage people who could afford to pay more to self-select out of the discount and provide the ISP more revenue.

Also — and this applies to most changes that the new NTIA leadership could make at this stage — the timing is awkward. At a time when some Final Proposals are already approved and subgrantee selection is well underway in most states, any policy change that would affect projects, funding requests, or competition risks creating inconsistencies and bait-and-switch problems at best.

Some changes might not even be feasible unless states backtrack and return to the planning stage. As time passes, these challenges will only be exacerbated as states charge forward while Washington considers its next move.

Rapid progress in the states

States are demonstrating BEAD momentum as never before. The number of states that have opened a project application window to date is 30 and counting. Other states are busy getting applicants prequalified, have clear timelines posted, and/or have released prequalification or project application materials.

A few states, such as Alabama, Florida, Maryland, and New Jersey, are focused on the challenge process and haven’t yet put in motion their processes for subgrantee selection. But in the vast majority of states, some stage of subgrantee selection is already underway.

Table 1 above shows the next 10 states’ Final Proposal deadlines, and most of the rest are due later in the summer or early in the fall. To meet the 14-day public comment requirement, with time to integrate feedback, Final Proposals should be posted at least three to four weeks before the NTIA deadline.

If all is on track, Final Proposals from Kansas, West Virginia, Washington, Pennsylvania, Colorado, and others should appear within the next few weeks at the latest. States can post them earlier if they are ready.

Kansas appears to be nearing that milestone. It closed its project application window on December 20, and in late January, it posted a summary of the Round 1 submission to its program website. Kansas received:

- 200 applications, for

- 50,209 BEAD-eligible locations, amounting to a

- 96% coverage rate, with

- $943 million in total proposed project cost, of which

- $673 million would be covered by BEAD, while

- $270 million in matching funds was proposed.

Kansas’s $451.7 million in BEAD funds isn’t enough to cover $673 million in grant requests. But some projects presumably overlap and therefore shouldn’t require $673 million in expenditures to achieve full coverage of the applied-for areas. In the end, Kansas’s BEAD funding may be sufficient to cover its need.

When a state faces a BEAD funding shortfall, it can 1.) shift toward the utilization of more cost-effective broadband technologies, 2.) find other funding sources to supplement BEAD, or 3.) refocus funds on unserved locations (lacking 25/3 internet service) while descoping some or all underserved locations (which have 25/3 but lack 100/20).

States will also need to strive to achieve universal coverage even when they get no applications for some eligible locations.

Washington State recently announced results from its first round of grant applications. It received 307 project applications, with 77% of broadband serviceable locations (BSLs) receiving at least one bid and 49% receiving two. Pennsylvania closed its first BEAD application round on February 7, having received 239 applications from 26 organizations, which jointly covered 97% of the eligible locations in the state. And Arkansas, reports overwhelming provider participation in its first BEAD round, with 98% of locations having received bids. A small number of “Buy It Now” bids that qualified for immediate acceptance covered 9% of BEAD eligible locations with 2% of Arkansas’s funding.

Achieving universal coverage will sometimes involve the use of “alternative technologies” — including unlicensed fixed wireless and LEO satellite services.

The last last-mile: LEO satellite and BEAD choice of technology

One feature of BEAD that hasn’t changed — yet, at least — is the “Guidance for BEAD Funding of Alternative Broadband Technology” the NTIA published on January 2, 2025. For now — unless the new NTIA leadership acts to scrap it — that guidance governs how states should use BEAD funds for the unlicensed fixed wireless and LEO satellite projects that will be needed in some of the remotest, hardest-to-serve locations.

In November 2021, when it passed the IIJA, Congress tasked the BEAD program with achieving universal broadband coverage. The economics of that are inherently challenging because deployment costs per location — at least for a given technology, such as fiber — surge exponentially as you push out to the hardest-to-serve locations. That’s why BEAD required so much planning; this is a particularly difficult problem to solve.

The irony is that during BEAD planning, the problem got solved — at least in a way. While Starlink existed in November 2021, its capacity trajectory was unknown. Since then, it has launched thousands of satellites, signed up well over a million subscribers, and begun to claim (in its reporting to the FCC) 100% U.S. coverage at the BEAD program’s 100/20 bandwidth goal. Some advocate “technology neutrality” for the BEAD program — i.e., treating LEO satellite like other broadband technologies. But if Starlink counts, BEAD arguably isn’t needed at all.

Others argue that technology neutrality doesn’t account for the inherent differences in service quality and reliability between LEO and fiber, and therefore, that BEAD should move forward to fund a great deal of end-to-end fiber deployment.

Fiber has a clear performance advantage over Starlink, providing the ability to deliver significantly higher bandwidth and lower latency connections. It is also upgradeable in the future by replacing the optical gear at each end of the fiber instead of requiring the replacement of the fiber itself.

Starlink has limited throughput capacity, and its delivery capacity gets “sold out” in areas of high demand. It stands to reason that Starlink, which is a constellation of non-stationary satellite overflights, will be less likely to get “sold out” if fiber meets much of the local need.

Another irony is that a new “massive MIMO” approach to wireless internet has begun to deploy services that claim fiber-competitive gigabit symmetric coverage. It can achieve this even using unlicensed spectrum because the technology is adept at working around radio interference.

Fiber still makes sense as a long-term bet where it can be affordably deployed — because it lasts for decades without using scarce spectrum resources or launching new satellites into space that have a limited shelf-life. But when fiber projects aren’t practical, it is encouraging that alternatives have improved.

The NTIA’s alternative technology guidance adapts to the last last-mile challenges with two key principles:

1. Where no “reliable” — fiber, cable, or licensed fixed wireless — projects are offered, but unlicensed fixed wireless (ULFW) coverage at 100/20 speeds is available, the ULFW provider will get a chance to prove it has capacity to meet the local needs. If it can, BEAD will treat the area as served.

2. Where there is neither a “reliable” technology BEAD project nor an incumbent ULFW provider, LEO satellite can be subsidized through “LEO Capacity Subgrants” that will pay LEO providers to “reserve capacity” for BEAD occupants with no other options.

The guidance will be difficult for states to implement, especially with so little time. But it meets a need. By verifying ULFW coverage claims and buying reservations of LEO capacity, NTIA has outlined a sensible way to close the loop on universal broadband coverage plans.

Conclusion: Flying through turbulence

While the change of administration has introduced some to-be-expected turbulence to the BEAD program, it is still in flight. Some of this turbulence may, in fact, turn out to be good for the program and the taxpayer. If the new leadership in Washington can strike the right balance (i.e., streamlining the program without disrupting it), then state broadband offices should be able to stay in flight until they land safely in a few months — with robust grant awards and the deployment of universal broadband coverage.

Millions of Americans are eagerly awaiting the end of Digital Divide, at least in terms of access. Let’s make some course adjustments, keep a steady hand on the controls, and reach our destination.

Dr. Nathan Smith, Director, Economics and Policy

Meet the author

Dr. Nathan Smith monitors federal broadband policy for Connected Nation. He also writes public comments for federal agencies that request advice on broadband policy implementation and helps with business development and proposals.